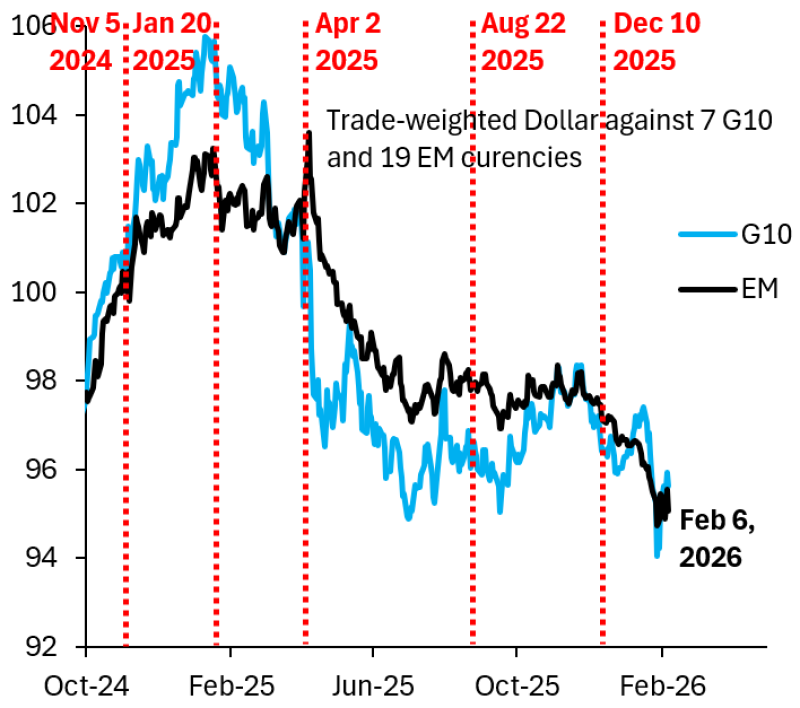

⬤ The US Dollar is weakening more noticeably against emerging market currencies than against its developed market counterparts. The Dollar versus emerging markets started showing real weakness right after the Federal Reserve cut rates on December 10, and the trend continues pointing downward.

⬤ Looking at the trade-weighted Dollar index, both the G10 (developed markets, shown in blue) and emerging markets (shown in black) peaked earlier around the 102 to 105 range. But here's the key difference: the emerging market index turned south earlier and dropped much faster. By February 6, 2026, the EM measure had tumbled to the mid-90s, while the G10 index followed the same path but at a slower pace.

⬤ "The Dollar versus emerging markets began signaling meaningful weakness after the Federal Reserve's rate cut on December 10 and continues to point toward further declines."

⬤ This gap tells us something important—emerging market currencies typically respond quicker to changes in global monetary policy. Once the Fed made that December 10 rate cut, the EM Dollar index dropped faster, showing broad Dollar weakness before developed market currencies caught on.

⬤ Why does this matter? Currency movements often give us early signals about shifts in global financial conditions. The Dollar's continued slide against emerging markets suggests easing financial pressure worldwide and points to more Dollar weakness ahead.